The holiday season ends here

There was an adage that stronger employment numbers were bad for equity markets and vice versa; why? Simply because strong employment indicated a strong economy, a higher risk of inflation and a reduced chance of cuts in interest rates or even possibly the possibility of central banks raising rates. I don’t confess to understanding what is going on in the US employment market; one week to the next, they seem to suggest something different. Anyway, on Friday, a very strong December jobs report sent yields higher, reflecting a further dent in hopes the Fed will be in mind to cut rates aggressively in the near future. The unemployment rate fell to 4.1%.

One economist at the Bank of America even suggested this report could force the Fed to look to raise interest rates. When quizzed on this point at the December meeting, Jerome Powell replied that ruling anything out in this world is unwise. The release of December Fed meeting minutes recorded that committee members were concerned about the potential impact the policies the president-elect is proposing could have on inflation. Reflecting this concern that inflation is proving sticky, the five- and 10-year break-even inflation rates have risen in the past months. Adding to inflation concerns will the recent rise in the price of oil, hitting a 3-month high. One has probably noticed the impact in the UK; a weaker pound and higher oil prices have pushed the price of petrol on the forecourt back above £1.4 a litre.

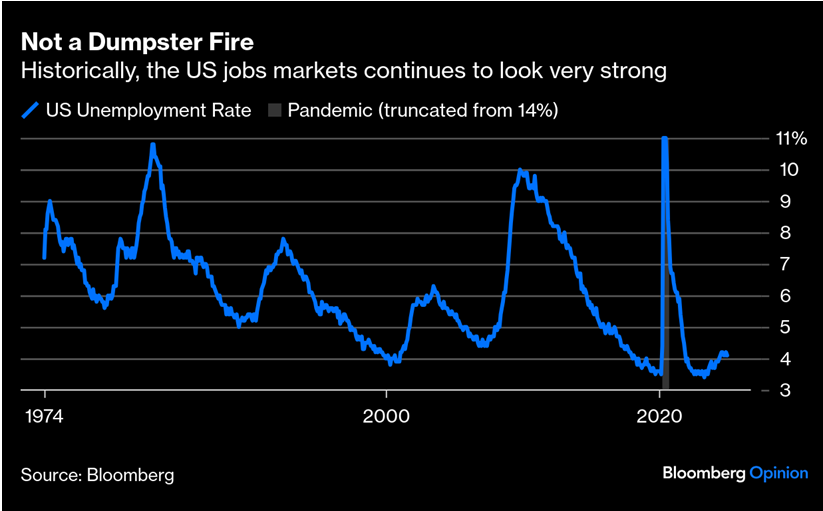

I have quoted Peter Berezin, BCA’s Chief strategist, who points out that once unemployment rates start to rise, they continue, possibly not in a straight line. This Bloomberg chart reflects that view.

This week’s focus will turn away from the economic backdrop to corporate earnings as we get the start of the fourth quarter earnings season at the end of the week, led by JP Morgan and several other leading global banks. Before that, though, another spanner could be thrown into the bond market as we get the monthly US CPI report. Estimates vary from year-on-year headline between 2.6 and 2.9%, with consensus at 2.7%.

The weekend press was full of reports on the current state of the UK economy, higher yields, and confidence in the Chancellor, which was all to be expected. Towards the end of the weekend, the rhetoric coming out of No11 was for the need for spending cuts. Spending cuts could hit economic activity again, but it could also make the Bank of England’s job slightly easier, as it may encourage them to look to ease monetary policy. If the market gains some confidence that the government is serious, this recent selloff may provide an opportunity to lock in higher yields for longer. It’s hard to get bullish on sterling, though. As well as the US, we get a raft of UK inflation data on Wednesday; markets expect the year-on-year rate to rise to 2.7%. Then, on Thursday, the monthly GDP report and a series of industrial and manufacturing reports. Ms Reeves will be hoping for some good news.